- December 8, 2025

- Eicrasoft

- 0

Starting a business is an adrenaline rush, but the first critical move is Business Formation. This isn’t just paperwork; it’s the legal cornerstone that defines your company’s existence, locking in your liability protection, ownership structure, and tax strategy. Choosing the right path—whether a Sole Proprietorship, Partnership, LLC, or Corporation—is the non-negotiable foundation that sets you up for strategic success and growth from Day One.

Key Takeaways

- Foundation First: The legal entity (LLC, Corp, etc.) is the framework that dictates your liability, taxes, and potential for growth.

- Scale Smart: Higher investment in formal entities means higher credibility and global scalability, essential for attracting investors and supporting remote teams.

- Non-Negotiable Compliance: Registration and licensing protect your business and are required for banking and RJSC (Registrar of Joint Stock Companies) compliance.

- Expert Advice Pays: Consulting attorneys and accountants is the most effective way to save money, minimize tax burdens, and align your structure with your long-term goals.

- Future-Proofing: Form your business thoughtfully to protect personal assets and maintain the agility needed to adapt to evolving markets.

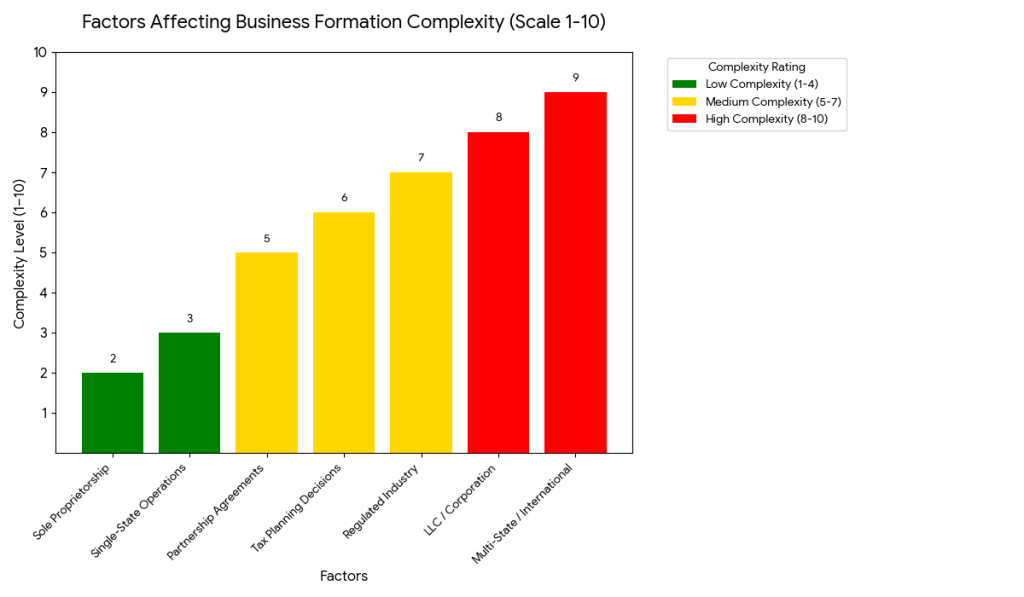

The Challenges and Factors of Business Formation

Business formation can range from simple to highly complex—it largely depends on the choices you make and the structure you select. Here’s what influences the difficulty level:

- Business Entity Type

- Sole proprietorships are usually straightforward and easy to set up.

- LLCs and corporations involve more complexity, requiring formal registration, operating agreements, and ongoing compliance documentation.

- Sole proprietorships are usually straightforward and easy to set up.

- Legal Scope

- Operating in a single state is simpler.

- Multi-state or international operations require navigating different legal, licensing, and tax regulations, which increases complexity.

- Operating in a single state is simpler.

- Industry Regulations

- Highly regulated industries like healthcare, finance, or food services have specific licensing and compliance requirements that add additional layers of complexity.

- Highly regulated industries like healthcare, finance, or food services have specific licensing and compliance requirements that add additional layers of complexity.

- Tax Considerations

- Choosing between corporate taxation and pass-through taxation for LLCs or partnerships affects both your financial planning and administrative burden, influencing how complex the setup will be.

- Choosing between corporate taxation and pass-through taxation for LLCs or partnerships affects both your financial planning and administrative burden, influencing how complex the setup will be.

- Partnership Agreements

- Partnerships, even small ones, need clear agreements outlining roles, responsibilities, profit sharing, and decision-making processes, adding legal and operational detail to the formation process.

Optimizing Taxes & Financial Planning

- Choose the Right Entity: LLC, S-corp, or partnership—pick what fits your goals.

- Use Pass-Through Taxation: Avoid double taxation by passing income to personal returns.

- Maximize Deductions: Claim business expenses, home office, and retirement contributions.

- Offer Tax-Friendly Benefits: HSAs, 401(k)s, and FSAs reduce taxable income.

- Track Expenses: Keep records to claim every deduction.

Navigating Business Challenges: A 7-Step Action Plan

A systematic approach ensures sustainable operations and growth by tackling formation and operational issues head-on:

- Define the Problem: Clearly identify and articulate the specific challenge (e.g., “high liability risk,” “inefficient mail processing”).

- Gather Data: Collect all relevant information—review contracts, financial records, and current operational processes.

- Seek Expertise: Don’t guess. Consult attorneys for legal structure, accountants for tax strategy, or industry specialists for operations.

- Engage the Team: Solicit input from employees; they often have valuable, practical insights into daily friction points.

- Develop a SMART Plan: Create goals that are Specific, Measurable, Achievable, Relevant, and Time-bound.

- Allocate Resources: Dedicate the necessary time, budget, and personnel to execute the plan successfully.

- Implement & Adjust: Execute the solutions systematically, continuously monitor the results, and be ready to adapt the strategy as needed.

Our Business Formation Services

We help entrepreneurs in Bangladesh set up and grow their businesses smoothly:

- Entity Registration: Sole Proprietorship, Partnership, LLC, or Corporation; name reservation & official filings.

- Legal & Compliance: Licenses, permits, corporate governance, and regulatory compliance.

- Tax Planning: Tax structure selection, VAT registration, deductions, and optimization.

- Expert Advisory: Attorneys and accountants guide you on liability, contracts, taxes, and growth.

Focus on growing your business while we handle the legal, compliance, and financial setup!

Seeking Expert Advice: Attorney vs. Accountant

When forming or structuring your business, different professionals handle different parts of the foundation. Here is a table clarifying when you should consult an Attorney versus an Accountant for critical advice:

| Focus Area | When to Consult an Attorney (Legal Expert) | When to Consult an Accountant (Financial Expert) |

|---|---|---|

| Business Entity Choice | Primary: To determine the best legal entity (LLC, Corp) for liability protection and asset separation. | Secondary: To advise on the tax implications of that choice (e.g., S-Corp election). |

| Foundational Documents | Primary: Drafting the Operating Agreement (LLC), Bylaws (Corp), or Partnership Agreements. | N/A (This is purely a legal drafting function). |

| Compliance & Registration | Primary: Handling official state/federal registration, ensuring legal compliance, and acquiring necessary permits. | Secondary: Setting up internal financial compliance and bookkeeping systems. |

| Tax Strategy | Secondary: To understand legal tax requirements for the entity type. | Primary: Developing the overall tax strategy, optimizing deductions, and setting up tax filing procedures. |

| Contracts & Agreements | Primary: Reviewing leases, vendor contracts, and client/employee agreements. | N/A |

| Operational Setup | N/A | Primary: Establishing the Chart of Accounts, setting up payroll, and managing long-term financial forecasting. |

Conclusion

Forming your business is more than a starting point—it’s the cornerstone of long-term success. By diligently selecting the right structure, you gain liability protection, operational clarity, and crucial financial efficiency. Whether you choose a Sole Proprietorship or an LLC, strategic planning and expert guidance are essential. Focus on your vision while professionals ensure your structure is legally compliant and perfectly positioned for sustained growth in the dynamic Bangladeshi market.

FAQ (Frequently Asked Questions)

The common options are sole proprietorships, partnerships, LLCs, S corporations, and C corporations.

A sole proprietorship is unincorporated and puts personal assets at risk, while an LLC provides limited liability protection and typically features pass-through taxation.

Consider your goals, how much liability protection you need, tax implications, and how you want to manage the business. It’s wise to consult legal and financial professionals.

Yes. The right entity choice, plus eligible deductions and tax-advantaged structures, can improve tax efficiency.

Timing depends on the entity type and your jurisdiction, ranging from a few hours to several weeks.

Follow Us:

📱FB:https://www.facebook.com/Coworking.BD

🐦Twitter: https://x.com/host_bd1

📸Linkedin:https://www.linkedin.com/company/host-com-bd

💼Insta: https://www.instagram.com/host_bd1/

▶️Youtube:https://www.youtube.com/channel/UCpTJMuoM6mNAAbqOVq6MDOw